African Gold Market 2025: Trends, Opportunities, and Insights

The African Gold Market is a powerhouse in global gold production, driving economic growth and investment opportunities across the continent.

In 2024, Africa produced over 850 tons of gold, accounting for nearly 30% of the world’s supply, with South Africa, Ghana, and Mali at the forefront.

This guide dives into the latest market trends, untapped investment potential, and critical challenges shaping the industry in 2025.

Whether you’re an investor eyeing gold stocks, a researcher studying mining impacts, or curious about Africa’s role in global trade, this article delivers actionable insights and up-to-date data.

From rising demand to sustainability concerns, we explore what makes the African gold market a focal point for global stakeholders.

Read on to discover opportunities, risks, and the future of this dynamic industry.

Overview of the African Gold Market

The African Gold Market is a cornerstone of the global gold industry, driving economic growth across the continent and significantly contributing to the world’s gold supply.

In 2024, Africa accounted for approximately 27% of global gold production, producing over 690 metric tons valued at roughly $47 billion, fueled by major producers like Ghana, South Africa, and Mali.

This robust gold mining sector underscores Africa’s geological wealth, particularly in West Africa and South Africa’s Witwatersrand Basin, positioning the continent as a key player in meeting global demand for jewelry, investment, and technology.

The economic impact on African economies is profound. Gold exports generate substantial foreign exchange earnings, with South Africa’s net export surplus reaching $7.1 billion and Ghana’s $5.65 billion in 2024.

In Ghana, gold accounts for over 30% of export revenue, supporting jobs and infrastructure development.

However, challenges like illegal mining and environmental degradation persist, with Ghana’s “galamsey” polluting over 60% of water bodies.

Despite these hurdles, investments in local refining, such as Ghana’s new $110 million refinery, enhance value addition and reduce reliance on foreign processing.

The African gold market’s strategic importance is further amplified by rising global prices, reaching $2,464 per ounce in 2024, driven by economic uncertainty and central bank demand.

As Africa navigates sustainability and governance challenges, its gold sector remains vital to both regional prosperity and global supply chains.

Major Gold-Producing Countries in Africa

Africa’s gold mining industry is a global powerhouse, with key nations driving significant African gold production in 2024.

The continent’s African gold market thrives on rich deposits, notably in West Africa’s Birimian belt and South Africa’s Witwatersrand Basin.

Below, we explore the top gold-producing countries—South Africa, Ghana, Mali, Burkina Faso, Sudan, and Uganda—highlighting their contributions, challenges, and key players.

South Africa: Historical Dominance and Modern Challenges

South Africa, once the world’s top gold producer, peaked at 995 metric tons in 1970 but produced ~100 metric tons in 2024.

Declining shallow reserves and ultra-deep mining challenges (e.g., Mponeng mine, over 4 km deep) raise costs, compounded by energy shortages and illegal “zama zamas” mining.

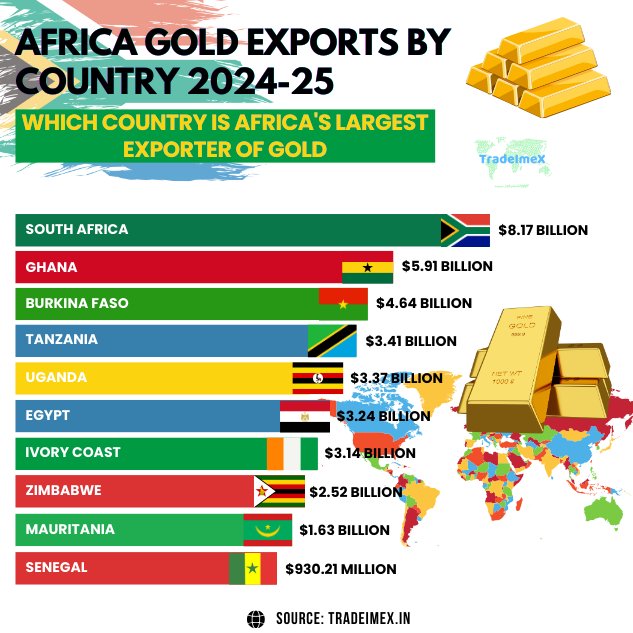

Companies like Harmony Gold, Gold Fields, and Sibanye-Stillwater accounted for 76% of output in 2022, with exports valued at $8.17 billion in 2024.

Ghana: Africa’s Top Gold Producer

Ghana, the “Gold Coast,” became Africa’s leading producer with ~127 metric tons in 2024, driven by Birimian greenstone belts and mines like Ahafo (Newmont, 798,000 oz) and Tarkwa (Gold Fields).

Gold generates 57% of export earnings ($11.6 billion), supported by artisanal mining (30% of output) and projects like Cardinal Namdini (350,000 oz by mid-2025). Illegal “galamsey” mining, however, pollutes water bodies, challenging sustainability.

Mali, Burkina Faso, Sudan, Uganda: Emerging Markets

Mali’s 67.7 metric tons in 2024 came from mines like Loulo-Gounkoto (Barrick Gold, 723,000 oz) and Fekola (B2Gold), contributing 75% of export revenue, though political instability and a 2023 mining code pose risks.

Burkina Faso produced 57.6 metric tons via Bomboré (Orezone Gold) and Houndé (Endeavour Mining), but insurgent threats and nationalization (e.g., SOPAMIB’s Boungou acquisition) hinder growth.

Sudan’s ~50 metric tons, mostly artisanal from Hassai, supports 4% of GDP, yet smuggling and conflict disrupt trade.

Uganda, an emerging player, produced ~2.5 metric tons in 2024, with potential in Busia and Karamoja regions. New discoveries and policies like the 2022 Mining Act aim to boost output, but infrastructure and regulatory gaps limit scale.

Comparison of Major Gold-Producing Countries (2024)

|

Country

|

Production (Metric Tons)

|

Major Mines

|

Key Companies

|

|---|---|---|---|

|

Ghana

|

127

|

Ahafo, Tarkwa, Obuasi

|

Newmont, Gold Fields, AngloGold Ashanti

|

|

South Africa

|

100

|

Mponeng, Kusasalethu, South Deep

|

Harmony Gold, Gold Fields, Sibanye-Stillwater

|

|

Mali

|

67.7

|

Loulo-Gounkoto, Fekola, Syama

|

Barrick Gold, B2Gold, Resolute Mining

|

|

Burkina Faso

|

57.6

|

Bomboré, Houndé, Essakane

|

Orezone Gold, Endeavour Mining, IAMGOLD

|

|

Sudan

|

50

|

Hassai, Block 14

|

Sudan Gold Refinery, Artisanal Miners

|

Note: Production figures are approximate, based on 2024 data from sources like the World Gold Council.

Market Trends and Drivers

The African gold market is shaped by global demand, rising prices, and evolving policies, influencing gold mining and trade across the continent.

In 2024, Africa’s gold production reached ~690 metric tons, contributing 30% to global supply, driven by key trends and drivers outlined below.

Global Demand

Global gold demand surged 1% to 4,974.5 tons in 2024, valued at a record $382 billion. Jewelry, the largest sector, fell 11% to ~2,000 tons due to high prices, impacting African exporters like Ghana, where gold comprises 57% of exports.

Technology demand, particularly for AI-related applications, remained resilient, supporting African producers despite tariff pressures.

Investment demand, including ETFs and bars, rose 25% to 1,180 tons, fueled by central bank purchases (1,000+ tons for the third year) and high-net-worth investors seeking hedges against geopolitical risks.

Africa benefits as a key supplier, with Ghana and South Africa meeting ETF and bar demand.

Price Trends

Gold prices soared 27% in 2024, reaching $3,540.25/oz by September 2025, driven by trade uncertainty and a weaker US dollar.

The World Gold Council forecasts rangebound prices in H2 2025, with a 0–5% increase, potentially hitting $3,669.63 by year-end.

J.P. Morgan predicts $3,675/oz by Q4 2025, climbing to $4,000 by mid-2026, citing central bank buying (900 tons forecast for 2025) and ETF inflows.

These high prices boost African export revenues but challenge jewelry demand and artisanal mining profitability in countries like Sudan.

Policy and Regulation

Mining laws and trade policies significantly impact African gold production. Mali’s 2023 mining code, increasing state ownership, raised costs for firms like Barrick Gold, risking output declines.

Burkina Faso’s nationalization efforts, such as SOPAMIB’s Boungou acquisition, threaten investor confidence. Ghana’s GoldBod policy promotes local refining, enhancing value addition.

US tariffs in 2025, escalating trade tensions, indirectly raise gold prices by fueling safe-haven demand, benefiting African exporters.

However, smuggling in Sudan and illegal “galamsey” in Ghana undermine regulatory efforts, with 60% of Ghana’s water bodies polluted.

Investment Opportunities in the African Gold Market

The African gold market offers diverse African gold investments in 2025, driven by soaring gold prices ($3,540.25/oz in Sep 2025) and Africa’s 27% share of global production.

Investors can tap into this dynamic sector through stocks, ETFs, physical gold, and mining ventures, each with unique opportunities and risks.

Stocks and ETFs

Investing in gold mining stocks and ETFs provides exposure to Africa’s gold boom without physical ownership.

Major players like Barrick Gold (NYSE:B, $26.63 in Aug 2025), operating in Mali and Tanzania, reported a Q2 2025 EPS of $0.47, beating estimates, with a 2.1% dividend yield.

Newmont (NYSE:NEM), active in Ghana, produced 6.8 million ounces in 2024, benefiting from a low forward P/E of 8.4.

Africa-focused ETFs like the VanEck Gold Miners ETF (GDX, $14.2B AUM) include Barrick (8.3%) and Newmont (13.56%), offering diversified exposure.

Ghana’s Asante Gold Corporation, listed on the Ghana Stock Exchange, provides local market access. ETFs like GDX (0.51% expense ratio) are ideal for risk-averse investors seeking liquidity.

Physical Gold

Purchasing physical gold—bars or coins—offers tangible security, especially in hubs like Accra, Ghana, via dealers like the Precious Minerals Marketing Company (PMMC). Ghana’s $110M Gold Coast Refinery enhances local supply.

However, risks include storage costs, security, and liquidity challenges. High gold prices reduce affordability, and US tariffs (proposed in 2025) may impact import costs.

Physical gold suits long-term investors but lacks the leverage of stocks. Verify dealer credibility to avoid fraud.

Mining Ventures

Institutional investors can fund gold mining ventures in emerging markets like Uganda or Egypt, where Barrick is exploring new concessions.

Projects like Ghana’s Cardinal Namdini (350,000 oz/year by mid-2025) or Mali’s Loulo-Gounkoto offer high returns but face risks like Mali’s 2023 mining code or Burkina Faso’s nationalization.

Joint ventures, like Barrick’s Nevada Gold Mines (61.5% ownership), show potential for stable returns. Geopolitical risks and ESG concerns (e.g., Barrick’s $114,750 fine in Canada) require due diligence.

Call-to-Action: Consult a financial advisor Like Gold Buyers Africa for tailored investment strategies to navigate the African gold market’s opportunities and risks effectively.

Challenges and Risks

The African gold market faces significant hurdles that impact gold mining and African gold production. Despite its 27% share of global output in 2024, environmental, political, and illegal mining challenges threaten sustainability and profitability.

Environmental Impact

Gold mining’s environmental toll is substantial, particularly in Ghana, where illegal “galamsey” operations polluted over 60% of water bodies, per a 2024 Ghana Water Resources Commission report.

Mercury use in artisanal mining contaminates rivers, harming ecosystems and communities. Sustainable practices, like Newmont’s cyanide-free processing at Ahafo, aim to mitigate damage, but adoption is slow.

South Africa’s mine rehabilitation efforts, mandated by the 2018 Mineral and Petroleum Resources Act, address legacy pollution but face funding shortages, with only 10% of abandoned mines rehabilitated by 2024 (Creamer Media).

Political Instability

Political risks disrupt operations in emerging markets. Mali’s 2023 mining code, increasing state ownership, raised costs for Barrick Gold, reducing output by 5% in 2024 (World Gold Council).

Burkina Faso’s insurgent violence and nationalization (e.g., SOPAMIB’s Boungou acquisition) deter investment, with 30% of mining sites affected by security issues in 2024 (Reuters).

Sudan’s ongoing conflict disrupts artisanal mining, diverting 20% of production to smuggling (UN Report, 2024).

Illegal Mining

Illegal mining skews market dynamics, with Ghana’s galamsey costing $2.3 billion in lost revenue annually (Ghana Chamber of Mines, 2024).

In Sudan, smuggled gold bypasses formal markets, reducing GDP contributions. These activities undermine regulatory frameworks and investor confidence, destabilizing the African gold market.

Future Outlook for 2025 and Beyond

The African gold market is poised for dynamic growth in 2025 and beyond, driven by rising production, technological advancements, and global demand.

Below are key predictions shaping African gold production:

Rising Production in West Africa:

West Africa’s gold output is forecast to grow, with Ivory Coast and Niger leading emerging markets at a 3.1% CAGR through 2030, reaching 5.65 million ounces, per GlobalData.

Ghana’s Cardinal Namdini mine will add 350,000 oz annually by mid-2025, while Mali’s Loulo-Gounkoto expands output.

“West Africa’s geological potential and government incentives will drive gold production growth,” says John Reade, Chief Market Strategist at the World Gold Council.

Technological Advancements in Mining:

AI, satellite imagery, and blockchain are transforming gold mining. By 2025, over 60% of West African mines will adopt sustainable chemical processes, reducing cyanide use, per Farmonaut.

Automation, like Epiroc’s battery-electric loaders in DRC, cuts costs by 30% and emissions, boosting efficiency. “AI and digital tools will revolutionize exploration and ESG compliance,” notes Dr. Gargi Mishra, GMG-SAIMM Mining Innovation Thought Leader.

Sustainability and Challenges:

Stricter regulations, like Mali’s 2023 mining code, and rising ESG demands will push sustainable practices but may increase costs.

Illegal mining and geopolitical risks, particularly in Burkina Faso, could hinder growth, with a projected 1.5% CAGR decline in major markets by 2030.

These trends signal a robust yet complex future, balancing innovation with environmental and political challenges to sustain Africa’s global gold dominance.

Frequently Asked Questions (FAQs)

Which African country produces the most gold?

Ghana is Africa’s top gold producer, yielding ~127 metric tons in 2024, surpassing South Africa. Its Birimian greenstone belts and major mines like Ahafo (Newmont, 798,000 oz) and Tarkwa (Gold Fields) drive output. Gold accounts for 57% of Ghana’s export earnings ($11.6 billion), supported by artisanal mining and projects like Cardinal Namdini, set to produce 350,000 oz annually by mid-2025. Policies like GoldBod and local refining bolster its lead, despite illegal “galamsey” challenges.

How can I invest in the African gold market?

Investors can access the African gold market through stocks (e.g., Barrick Gold, Newmont), ETFs like VanEck Gold Miners ETF (GDX, $14.2B AUM), or physical gold via dealers like Ghana’s PMMC. Mining ventures in emerging markets like Uganda offer high returns for institutional investors. High gold prices ($3,540.25/oz in 2025) enhance profitability, but geopolitical risks and ESG concerns require due diligence. Consult a financial advisor to tailor strategies to your goals.

What are the risks of gold mining in Africa?

Risks in gold mining include environmental damage, political instability, and illegal mining. In Ghana, galamsey pollutes 60% of water bodies, per 2024 reports. Mali’s 2023 mining code and Burkina Faso’s insurgent threats raise costs and deter investment. Sudan’s smuggling diverts 20% of production. Sustainability issues and high operational costs (e.g., South Africa’s deep mines) challenge profitability. Robust ESG compliance and regulatory stability are critical to mitigate these risks.

Conclusion

The African gold market remains a vital force in global gold mining, contributing 30% of the world’s supply in 2024, valued at ~$47 billion. Countries like Ghana, South Africa, and emerging markets like Mali and Uganda drive economic growth through robust production and export revenues, with Ghana leading at 127 metric tons. Rising gold prices ($3,540.25/oz in 2025) and technological advancements, like AI-driven exploration, signal strong investment potential, despite challenges such as illegal mining and political instability.

As sustainability and local refining gain traction, Africa’s gold sector is poised for growth. Gold Buyers Africa Stay updated on gold market trends by visiting to our Platform to explore investment opportunities and industry insights.